There were 28 listed companies that disclosed their annual reports on April 6, 2017, including 8 GEMs, 6 small and medium-sized boards, and 14 main boards. There are 18 companies with rising performance.

Our financial research team selected five of the representative companies for financial review.

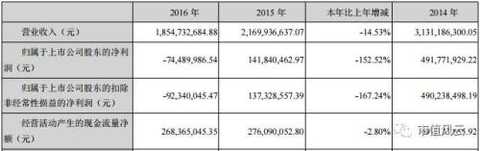

1. Sanonda A 000553, buy (000553.SZ)

The main accounting data and financial indicators are as follows:

Data map

The company is a large-scale chemical enterprise based on salt chemical industry, agricultural chemical industry as the main body and fine chemical industry. It is mainly engaged in the manufacture and sales of pesticides, chemical products and intermediates and import and export trade. The company's main products are pesticide chemical products, the main use is plant protection. The herbicide series mainly include glyphosate, paraquat, 2,4-D, etc.; the insecticide series mainly include acephate, dichlorvos, trichlorfon, carbofuran, methomyl, triazophos, etc.; The main series mainly include spermine, glyphosate, pyridine, etc. The main chemical products are caustic soda, liquid chlorine, hydrochloric acid and formaldehyde. During the reporting period, there was no major change in the company's production and operation model. The company's performance is greatly affected by the degree of prosperity of the agrochemical industry, bulk raw materials and pesticide prices.

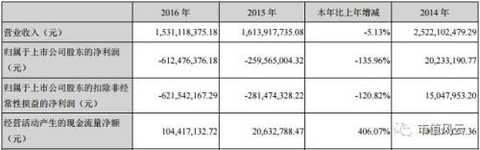

During the reporting period, the company realized:

The main reason for the decline in revenue and profit was: During the reporting period, the pesticide market continued to be sluggish. The sales prices of the company's main products continued to run at a low level, and the gross profit margin of sales decreased significantly. At the same time, the company promoted major asset restructuring and incurred a large amount of related agency fees.

The net cash flow from operating activities was basically the same as that of the previous year, with a slight decrease.

Fengyun Review

The company is listed on the market and is a company mainly engaged in the production and sales of pesticide chemical products. The company has the right to self-export; the proportion of the company's exports has risen, and the impact of exchange rate fluctuations on the company has increased. When signing a trade contract with a customer, the company should fully consider the exchange rate risk, settle the exchange at the spot, shorten the account period, adjust the structure of the export product, and adjust the risk in response to the tax refund policy.

Since 2014, the company's operating income and profit indicators have been declining year by year, and began to suffer losses in 2016. At present, the company's stock price is 14.73 yuan, and the price-earnings ratio is -117.45 times.

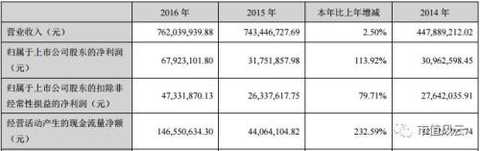

Second, Pioneer new material 300163, buy (300163.SZ)

The main accounting data and financial indicators are as follows:

Data map

The company is mainly engaged in the research and development, production and sales of polymer composite sunshade materials (sunlight fabrics). The company's main products are made of high-strength polyester yarn or glass fiber filaments and evenly coated with polymer composite materials. They are energy-saving, environmentally friendly, durable, and flame retardant. The company's polymer composite sunshade materials are in line with national strategy. Emerging industries, such as Aiki, net worth, and information development, belong to the new material industry, which is strongly encouraged by the state. Its products are used in building sunshade and have double-effect energy-saving effects, which can greatly reduce the electricity consumption for lighting and lighting. At the same time, it can be widely used in the construction industry and other industrial textiles.

2016 company realization:

During the reporting period, the company increased the integration of mergers and acquisitions enterprises, and the business status of the new M&A enterprises has been significantly improved. The loss of the Australian branch decreased by 69% compared with 2015. Gaither Auto Network turned profitable. At the same time, the company's domestic segment of the sun fabric sales business also showed a small increase.

The net cash flow from operating activities of the company increased by 232.59% compared with the previous year, mainly due to the decrease in the company's purchase payment during the year.

Fengyun Review

The company is listed on the market and is a high-tech enterprise engaged in the research and development of green, environmentally friendly and low-carbon building energy-saving polymer composite materials. The company's main products include polymer materials, composite materials, polymer composites, polyester, fiberglass and polyvinyl chloride.

Technological advancement and brand awareness are decisive barriers to participation in market share competition. Industry leaders with first-mover advantage have made forward-looking investments in product design, production process technology, and information application, further boosting entry into the industry. The competitive threshold; coupled with the horizontal and vertical integration of advantageous enterprises with capital advantages, they make them occupy most of the market share, and the survival of the fittest will be further accelerated. Other small and medium-sized domestic manufacturers mainly produce low-end products.

The domestic market is in its infancy, but it will also usher in a brutal competition. The company started the initiative of expanding the fabric to the sunshade finished product before the company. At the same time, the company introduced internationally renowned brands through overseas mergers and acquisitions, and further reduced production costs by opening up domestic and foreign production and sales, entering the downstream industries with higher profit margins, and further widening the leading gap with domestic counterparts. Since 2012, the company's operating income and various performance indicators have been increasing year by year, and its profitability has been continuously enhanced.

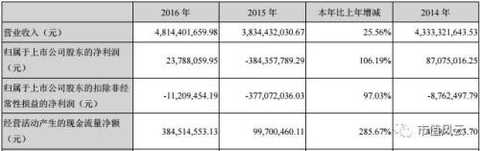

Third, Northeast Pharmaceutical 000597, buy (000597.SZ)

The main accounting data and financial indicators are as follows:

Data map

The company's main business covers chemical pharmaceutical (APIs, preparations), pharmaceutical business (wholesale, chain), medical engineering (medical design, manufacturing and installation), biomedical (biological diagnostic reagents) four sectors, forming a pharmaceutical upstream and downstream industries and services Cluster. The subsidiary company's import and export trading company mainly conducts import and export business and distribution of pharmaceuticals, and the company has a million-transportation company with dangerous goods qualifications, which can provide one-stop service for import and export trade. The company has a national Grade A pharmaceutical engineering design company and an equipment manufacturing and installation company with medical qualifications such as GC1 qualification and pressure vessel A2 qualification. It can provide supporting services for the company's internal medical design and equipment manufacturing and installation.

In 2016, the company achieved sales revenue of 4.814 billion yuan, a year-on-year increase of 25.56%; net profit attributable to shareholders of listed companies was 23.781 million yuan, a year-on-year decrease of 444.32 million yuan.

The reasons for the increase in performance are:

The net cash flow from operating activities was RMB 384.51 million, an increase of 285.67% over the same period of the previous year. This was mainly due to the increase in sales revenue during the period and the increase in cash received from sales of goods and services.

Fengyun Review

The company is listed on the market and is a company that manufactures and sells chemical raw materials and pharmaceuticals. The company is mainly engaged in the production and circulation of pharmaceuticals. During the 12th Five-Year Plan period, China's pharmaceutical industry has maintained a relatively high growth rate, but it has entered the 13th Five-Year Plan. With the weakening of growth momentum, structural contradictions have become more prominent, and the growth rate of future development will slow down. The reorganization and integration of the pharmaceutical industry has accelerated, the concentration has been continuously improved, and the pharmaceutical industry will be reshaped. At the same time, with the full implementation of the two-vote system in the pharmaceutical industry, channel resources are concentrated and collected, commercial companies accelerate the national layout, cross-regional integration, and the phenomenon of giants is gradually highlighted. The retail industry is facing major market opportunities in the new medical reform. The country's major pharmaceutical retail chain enterprises are accelerating their expansion and seizing resources. The future concentration and chain rate will be greatly improved.

The risks that the company should pay attention to in the future are: 1. Policy risks: reform of medical insurance payment methods, adjustment of new medical insurance catalogues, reform of public hospitals, two-vote system, implementation of reform of camps, promotion of graded medical treatment, etc., all of which will lead to the production, circulation and use of pharmaceuticals. The link has a major impact. 2. Risk of drug price reduction: With the implementation of the reform of medical insurance control fees and payment methods, the medical insurance payment price will become the wind vane for the reconstruction of the drug price system. In addition, the drug bidding will refer to the lowest price in each province, and the second bargaining of drugs will be released. Promote further reductions in drug prices.

In the past five years, although the company's operating income has remained at between 3.8 billion and 4.8 billion, the net profit is mostly at a loss, and after deducting non-recurring gains and losses, it is a continuous loss for five years.

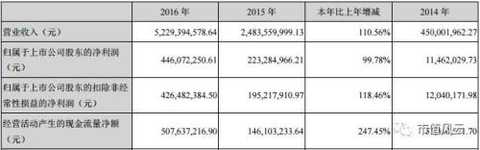

Fourth, Otto 002239, buy (002239.SZ)

The main accounting data and financial indicators are as follows:

Automotive air conditioning compressors, automotive air conditioning systems business and apparel business are the company's current main business.

During the reporting period, the company consolidated statements were implemented:

Overall, the company's 2016 business has maintained a good development trend, and revenue and profits have maintained rapid growth. Specific circumstances of each main business:

unit: yuan

Data map

During the reporting period, the company's cash flow from operating activities, cash outflow from operating activities and net cash flow from operating activities increased by 121.85%, 113.67% and 247.45%, respectively. The main reasons were: on the one hand, the company's subsidiary Nanjing Aotejia, Air Conditioning International ( The Group) and Fortis Air Conditioning were different from the previous year's accounting statements. On the other hand, the company's subsidiaries grew rapidly.

Fengyun Review

The company is listed, the company's current main business is automotive air conditioning compressors and automotive air conditioning systems business. In 2016, the sales growth rate of the company's automotive air-conditioning compressors was 10.3 percentage points higher than the growth of domestic automobile sales, indicating that the company's products have strong market competitiveness, and its market share and market share continue to increase.

Risks that the company may encounter in its future development:

V. Shandong Molong (002490.SZ)

The main accounting data and financial indicators are as follows:

Data map

During the reporting period, the company was mainly engaged in research and development, production and sales of products required for the energy equipment industry. The main products include oil and gas pipelines, fluid and structural pipes, pumping units, oil pumps, sucker rods, cylinder liners for drilling rigs, Valve parts and large castings and forgings. The company's products are mainly used in oil, natural gas, coalbed methane, shale gas and other energy drilling, machining, urban pipe network and other industries. The sales of tubular products exceed 80%, which is the main source of income and profit of the company. During the reporting period, the company's main business composition has not undergone major changes.

During the reporting period, the company realized:

According to the company's annual report, the reason for the decline in performance is: in 2016, affected by the economic situation, market demand declined, competition intensified, although there was a recovery at the end of the year, it was still operating at a low level, affected by fluctuations in oil prices and fluctuations in raw material prices, although production and sales were relatively The growth in 2015, but the product sales price fell sharply and the price fluctuated frequently, which led to a significant impact on the company's operating results.

The net cash flow from operating activities increased by 406.07% compared with the same period of last year, mainly because the company increased the amount of cash back in the current period and increased the cash inflow; the tax paid decreased, and the small loan company reduced the cash outflow compared with the increase in the last year . The reason is that the net cash flow from operating activities increased compared with the same period last year.

Fengyun Review

This loss-making company, the market value of the past, has been grievous and sent a "檄文" (檄文! Shandong Molong "bad huge losses", all directors Gao please bear joint responsibility)

The article is described as follows:

“ On February 3, the listed company Shandong Molong (002490, SZ) issued a revised performance announcement, stating that the company’s net profit attributable to shareholders of listed companies in 2016 is expected to be a loss of 480 million yuan to 630 million yuan. In the quarterly report, Shandong Molong had expected the net profit for the period from January to December 2016 to be between RMB 6 million and RMB 12 million, which turned losses into profits.

This final amendment is really accurate. Before that, the expected loss of profit is caused by the loss of investors. Who is going to go? Before the amendment, the major shareholder frantically reduced his holdings, and after he cashed in, he made a performance correction and used everyone as a monkey.

In view of Feng Yunjun, this anti-day performance correction has been far from the scope of financial accounting. Listed companies have been suspected of multiple violations and have already humiliated the IQ of all securities companies.

Sequin Fabric,Cheap Sequin Fabric,Sequin Lace Fabric,Multicolor Sequin Fabric

shaoxing rongxi textile co.,ltd , https://www.rongxifabrics.com