In all advanced economies, nominal wages have barely increased; interest rates have been at historically low levels for a long time; world population growth has slowed, and several major countries have shown negative growth? All of this indicates that long-term economic stagnation has arrived.

Even more frightening is that the central bank’s management and regulation of the economy is dying. From zero interest rate to quantitative easing to negative interest rate, it can be said that it is from an invalid policy to another invalid policy. Turning to a negative interest rate policy will not bring a significant economic driver in the long-term slow recovery of the global economy. On the contrary, it will only increase financial risks and make the next crisis possible.

The central bank with negative interest rates believes that traditional monetary policy is no different from non-traditional monetary policies such as quantitative easing and negative interest rates. This kind of cognition is problematic.

The reality is that in the economies that have been hit by the economic crisis, neither the wealth effect nor the exchange rate effect can promote the economic recovery and recovery. Instead, it has created new imbalances and become unstable factors. It is likely that the global economy will continue to be affected by a series of crises. sleepy.

There is no need to remain pessimistic about the prospects of the Chinese economy, but the large fluctuations in the Chinese securities market and the foreign exchange market cannot be taken lightly. Since last year, the sharp depreciation of the renminbi has also triggered a capital outflow from China. In fact, the net outflow of RMB in this round is the third round of net outflow in history.

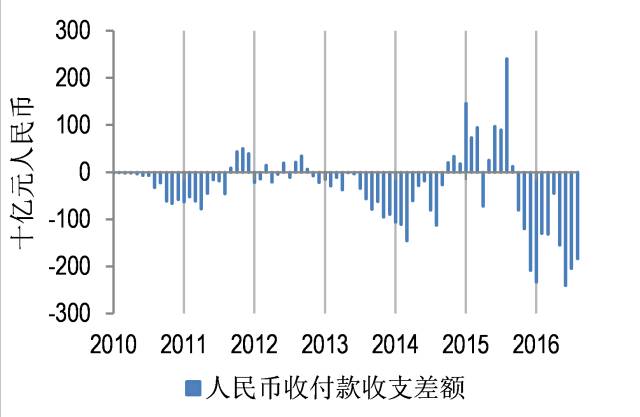

During the 11-month period from October last year to August this year, the RMB has been net outflows for 11 consecutive months, totaling 1.7 trillion yuan.

1

Roach: Negative interest rates lead to the next crisis

In the period of global stable growth for more than 20 years before the 2008 financial crisis, the development of macroeconomic theory was relatively slow, and the macroeconomic regulation and control of various countries was mostly “doing nothingâ€. Since the crisis, in order to get out of the recession, countries have regained their macro-control tools. In the macroeconomic theory, new terms such as quantitative easing, zero lower bound interest rates, and forward-looking guidance have emerged, and the practice of macro-control has also added rich content. A few days ago, "China Economic Report" reporters Wu Si and Li Dazhao interviewed Yale University professor and former Morgan Stanley chief economist Stephen Roach on foreign experience in macro-control and its reference to China.

China's economic report : After the 2008 financial crisis, we saw that the government's policy tools are becoming less and less. It is difficult to regulate the economic operation by traditional macro policies such as raising interest rates and interest rates. Some countries even enter the era of negative interest rates. What do you think about the current implementation of monetary policy in major developed economies?

Stephen Roach: The central bank’s management and regulation of the economy is dying. From zero interest rate to quantitative easing to negative interest rate, it can be said that it is from an invalid policy to another invalid policy. Zero interest rates and quantitative easing are powerful antidote to the weak market, but ultimately proved to be ineffective in repairing balance sheet vulnerabilities and stimulating a substantial recovery in aggregate demand. Similarly, the shift to a negative interest rate policy will not bring significant economic drivers in the long-term slow recovery of the global economy. On the contrary, it will only increase financial risks and make the next crisis possible.

The biggest problem with the above policy is to ignore the essential reasons for the global economic downturn in the post-crisis period. For the economies affected by the crisis, the focus should be on the demand side, and it is only when the company repairs its liabilities that it can end the balance sheet recession. In the case that monetary stimulus has largely been ineffective, the repair of the balance sheet is preceded by the recovery of aggregate demand.

China Economic Report: Why is negative interest rate making the next crisis possible?

Stephen Roach: The negative interest rate policy was first introduced in Europe in 2014 and recently adopted in Japan. It is an important change in the central banks of major economies in recent years. In the past, monetary policy focused on increasing aggregate demand by reducing borrowing costs and using wealth effects. The current negative interest rate policy is to stimulate the economy from the credit supply side by imposing "penalties" on the reserves deposited by the banks in the central bank. In other words, banks are encouraged to issue new loans regardless of actual loan demand. The central bank with negative interest rates believes that traditional monetary policy is no different from non-traditional monetary policies such as quantitative easing and negative interest rates. This kind of cognition is problematic.

In traditional monetary policy, the transmission mechanism mainly affects the physical sector through the loan interest rate. The demand for these sectors will change according to changes in the benchmark interest rate, especially in the entity sector that is sensitive to credit prices. The impact of interest rate adjustments is quickly transmitted to the entire economy, and this effect is often boosted by rising asset prices. In non-traditional monetary policy, the transmission mechanism mainly plays a role through the wealth effect of the asset market.

A number of risks are worthy of caution. For example, policymakers may be dependent on a bubbled financial market and are less willing to use fiscal stimulus to fall into a liquidity trap. Due to the lack of fiscal stimulus, the central bank can only continue to inject more liquidity into the bubble financial market, increasing the risk of financial instability. In addition, under the excessively loose monetary policy of the central bank, funds flowed into the financial market in large quantities, and there were a lot of bubbles in the stock market and the bond market, and the real economy was seriously distorted. When the bubble bursts, the unbalanced economy enters the balance sheet's recession, and the central bank that is pegged to inflation has “struck outâ€.

China's economic report: The Fed began to enter the interest rate hike cycle last year. Every time the interest rate hike will trigger global speculation and market volatility, what do you think?

Stephen Roach: Experience has shown that the excessive liquidity brought about by progressive normalization can easily lead to financial market exposure. These risks are even more worrying as the normalization process will be longer. The longer the Fed’s gradual rate hike process, the harder it will be and the greater the systemic risk. Only a very independent central bank can get the real economy out of dependence on financial markets. However, the Fed, caught in the debate on politicized economic growth, cannot afford this function. Only by shortening the normalization time will the Fed be able to reduce systemic risks. The sooner the Fed moves to the market, the smaller the market's impact on the economy. Admittedly, there are certain problems with the steep normalization path, but it is much better than another catastrophic crisis.

China Economic Report: While adjusting the short-term interest rate, the Fed is also using forward-looking guidance to stabilize medium- and long-term interest rates to ensure consistency, forward-looking and sustainability of monetary policy. How to better play the role of expected guidance?

Stephen Roach: On the whole, the risk of policy inconsistency is becoming more prominent. Trade-offs between strategy and tactics, long-term and short-term trade-offs exist in most economies, both developed and developing. This requires changing the macroeconomic policy framework, such as a clearer and more transparent arrangement of policy objectives, and avoiding conflicts between the objectives of different policy agendas. Furthermore, the central bank should independently formulate financial and monetary policies.

China's economic report: The proliferation of liquidity has become a global problem, and countries should rely more on fiscal policy than on competitive easing monetary policy. What advice do you have for how to better play the role of fiscal policy?

Stephen Roach: The fiscal stimulus must have an exit mechanism. In my opinion, the government's poor exit policy in terms of monetary and fiscal policies in the post-crisis period may also have an impact on the global economy. Regardless of whether it is the central bank or the financial sector, it is necessary to resolve the exit of special stimulus policies.

China Economic Report: What do you think are the main problems of the macroeconomic regulation and control policies of the countries after the crisis?

Stephen Roach: Since the financial crisis, the United States and other countries should be vigilant. If the economy is not controlled and structural reforms are not implemented, the economy will not be able to embark on a healthy recovery path, which may lead to more asset bubbles, financial crisis and Japan. Long-term stagnation. For example, in Japan, the reason why Japan succeeded in economic myth after World War II was mainly because the yen exchange rate was depressed. However, the suppression of the exchange rate is unsustainable. In the 1985 Square Agreement, Europe and the United States questioned the Japanese practice. Subsequently, the Bank of Japan had to implement a radical monetary easing policy, which led to a large-scale asset and credit bubble. In the end, the bubble burst, and the Japanese economy quickly entered a decline. Today, Japan is still suffering from economic imbalances.

Despite Japan’s tragic failure as a guide to the past, the rest of the world still insists on correcting structural problems with monetary policy. After 2008, the United States, Europe, and Japan quickly introduced quantitative easing policies. However, in addition to affecting the recovery of individual economies, this policy has also led to a sharp rise in the price of the securities market and a decline in the currency exchange rate, resulting in a broader systemic risk. As central banks inject large sums of money into the market one after another, the risk of asset bubbles in the world is intensifying, and national currencies are also likely to depreciate competitively. On the other hand, national policy makers are erroneously satisfied with the status quo and lack the motivation to solve structural problems.

Under the quantitative easing policy, countries continue to inject liquidity, and the monetary policy transmission mechanism shifts from interest to assets and foreign exchange markets. Proponents of non-traditional monetary policy say this is not a fear, because what the central bank can't do in the traditional way can now be achieved through the wealth effect of the asset market bubble or by lowering the exchange rate. However, the reality is that in the economies that have suffered from the economic crisis, neither the wealth effect nor the exchange rate effect can promote the economic recovery and recovery. Instead, it has created new imbalances and become unstable factors, which may cause the global economy to continue to suffer from a series of crises. Trapped.

China Economic Report: How do you judge the current economic situation in China?

Stephen Roach: There is no need to remain pessimistic about the prospects of the Chinese economy, but the volatility of China's securities market and foreign exchange market cannot be taken lightly, especially considering the commitment of China's market-oriented reforms. China is constantly pushing for structural adjustment. Some factors, such as the bursting of the stock market bubble, the dilemma of monetary policy, and the massive outflow of capital, will not have a decisive impact on the Chinese economy. China is entering a market-driven consumer society, and its financial infrastructure will continue to improve. Therefore, as China transitions to a new growth model, the mismatch between the economic rebalancing and the lag in financial reform will eventually be resolved. In the short term, the lag in financial reform does not mean an imminent crisis. China has huge foreign exchange reserves, which provide an important buffer against traditional currency and liquidity crises. Of course, if China's foreign exchange reserves continue to decline at a rate of $500 billion in 2015, then this buffer will disappear after six years. At present, China's foreign exchange reserves are more than 20 times that of 1998. I think this kind of pessimism will not happen.

2

Former US Deputy Secretary of State: How to deal with long-term economic stagnation

The author is a professor of economics at Harvard University and a former US Deputy Secretary of State. Wang Yizhen translation

Long-term economic stagnation refers to long-term slow economic growth below expectations, with particular concern for long-term economic zero growth or low growth. Is the global economy entering an era of long-term economic stagnation? What does this mean? This article will explore the causes and responses to the long-term stagnation of the global economy.

The cause of the long-term stagnation of the global economy

There are two reasons for the slow economic growth: either limited economic growth potential or weaker aggregate demand leads to a slowdown in output growth. Slow growth is possible, for example, when the capital stock is optimal, when the labor growth is zero or even negative, and the technological innovation is slow, unable to compensate for the negative growth effect of labor. In addition, everyone's desire for leisure will increase GDP growth, but the happiness index will not decrease.

If total demand growth is slow or does not increase, long-term stagnation may occur even if the economy still has potential production capacity. Because of weak demand, involuntary unemployment and overcapacity may result. If the willingness to save exceeds the investment, it will lead to insufficient aggregate demand.

1. Supply bottlenecks. The "long-term stagnation theory" was proposed and promoted by Alvin Hansen, a professor of economics at Harvard University in the late 1930s. Hansen's research focuses on the American economy of the 19th century. At that time, the economic power of the United States originated from the industrialization demand and housing requirements caused by the Westward Movement, railway construction, and rapid population growth (including local residents and immigrants), and the introduction and transportation of electricity in the later period. However, he is worried that with the weakening of these factors and the increase in corporate savings caused by policies such as the deposit insurance system and the corporate depreciation subsidy system, the US economic growth momentum will be insufficient and the economy may be stagnant. He is also worried that the capital investment that technology change can drive is becoming less and less. To be sure, he wrote this in the context of the Great Depression of 1929-1938, but he made it clear that he was solving long-term problems, not just a recognized long-term recession.

Hansen believes that there may be significant prosperity after World War II, but there will be a long-term depression followed. But he ignored the need for post-war baby boomers and the massive suburban housing and road construction needs brought about by the prevalence of affordable cars.

Gordon described the reasons for the economic stagnation and believed that the main factor affecting the long-term economic growth of the United States is not the lack of aggregate demand, but the supply bottleneck. Like Hansen, he places special emphasis on innovation and innovation, such as innovation in the fields of railways, power and internal combustion engines, and the petroleum industry. He proposed several factors limiting the growth of the United States: (1) population, the baby boomers gradually retired (and also live longer) from 1946 to 1960, but did not have enough young labor to replace them; (2) education, average education in the United States The level is difficult to upgrade, the cost of higher education is rising, the contribution of human capital to growth will be reduced; (3) inequality will increase; (4) the development of globalization will affect the actual wages of the United States; and (5) the strengthening of environmental supervision. These factors will further reduce the average annual growth rate of US household consumption to 0.2% in the future - this growth rate is similar to the 400-year consumption growth level before the British Industrial Revolution.

Some of Gordon’s correct views are acceptable: in economic growth, supply-side problems may lead to future economic stagnation. However, it is worth noting that Gordon is measured within the framework of national economic accounting, and there are serious shortcomings in the future. First, the output structure of the economy is changing. Over time, as many activities increase and some activities decrease, growth is the weighted average of all these changes, so the way in which the growth of the economy is valued is There are defects. Second, improvements in education and health care may not increase productivity, but there is no doubt that living standards will improve.

2. Insufficient total demand. Another explanation for long-term economic stagnation is insufficient aggregate demand, high unemployment and overcapacity leading to lower production capacity. How does this continue? In the savings investment identities of macroeconomic theory, savings and investment are equal. But usually, savings will far exceed investment. This unbalanced state leads to a reduction in effective demand. In a closed economy, excess savings can cause interest rates to fall, which can reduce savings and increase investment. However, in the actual economic operation, this ideal adjustment may not be realized for many reasons. For example, different departments have different flexibility for long-term interest rates, and investment in countries lacking mature mortgage markets is not sensitive to interest rates.

If interest rates cannot regulate savings and investment, what can be adjusted? Only rely on the adjustment of the overall level of economic activity, because it can just meet the equilibrium point of expected savings equal to the expected investment. But if the economy runs below growth potential and lasts for a long time, it will lead to long-term stagnation. The most typical example is Japan, which has experienced very slow growth since 1990. This process lasts for 20 years (Japan's growth potential is also affected by demographic factors, but this impact is almost zero).

Even if the investment is sensitive to interest rates, interest rates may be difficult to play, resulting in a fall in interest rates that cannot balance savings and investment. Since 2007, short-term interest rates in developed economies have been almost zero, and long-term interest rates have been at historically low levels. Low interest rates can no longer guarantee output or even maintain long-term economic growth, and are not enough to stimulate investment. Of course, as the life expectancy of residents increases, low interest rates may increase the actual income after retirement, thereby increasing savings. But in a closed economy, the household sector, the corporate sector, and the public sector cannot all be net savings.

The result of long-term economic stagnation is the waste of labor resources, the increase in long-term unemployment, the slow growth of capital stocks, the inability of young people to obtain jobs, and the fact that productive investment is lower than full-employment. As a result, potential output declines and potential production capacity will stagnate over time.

3. Global savings surplus. The discussions so far have been in a closed economy, which is not in line with the current world situation. At present, the world economy is increasingly globalized, and almost all economies have carried out extensive foreign trade, and many of them are very open. In this case, the balance of payments can be achieved through foreign trade. Small economies have no problem balancing their balance of payments in global trade, at least for the most part. Large economies are more difficult because long-term domestic stagnation may have a global spillover effect, as Ben Bernanke proposed the “global savings surplus†theory. Moreover, a country’s policy of dealing with excess savings does not apply to the global situation.

In fact, most of the world's large and medium-sized economies have account surpluses in 2015, suggesting that the risk of long-term stagnation is ubiquitous. We can infer that there is a general excess of savings in most large and medium-sized countries, even in China, which has a fairly high level of investment and a significant reduction in current account surplus.

The United States plays a special role in the distribution of world savings and investment, as most countries’ official reserves generally hold dollars. There have been several notable features of the US economic development in recent decades. First, capital prices, especially equipment prices, are not rising as fast as other prices, so a certain amount of savings will generate more substantial investment. This may also apply to other countries, and equipment becomes an important part of productive investment. Second, the US capital stock is slower than the actual output, so the overall capital output rate has been declining, in stark contrast to most of the past two centuries. Third, net investment has been declining for nearly 50 years. Of course, due to the impact of new technologies over the years, even if the capital stock does not increase, production capacity can grow. For all these reasons, we can say that the US current account deficit, the United States from the world's other countries to absorb excess savings, will not become productive investment, but become household consumption (including housing, national economic accounting investment) and public sector expenditure .

How is the United States that continues to have a current account deficit financed? Contrary to the usual impression, the US financing is not primarily through the acquisition of dollar assets by global central banks. US assets and securities are all that private investors around the world want, and even prior to their domestic investment. This of course includes high liquidity and low risk US Treasury bonds, as well as the equity of promising startups. In a nutshell, compared with other countries in the world, the United States has an advantage over other countries in stimulating new assets. Foreigners are more willing to buy, thereby promoting employment creation and driving the development of goods and services in the United States.

The world population is undergoing a slow change. World population growth has slowed and even negative growth has occurred in several important countries. The life expectancy is increasing, the average age of the country is growing, and the population over 70 is expected to rise sharply. Savings and investment are also cyclical, although there may be significant differences in each country. At the peak of the career, in addition to raising children, they usually plan for their retirement. As the average age rises, the total savings account is expected to rise. Although the strict life cycle hypothesis is violated, the total savings of retirees seems to Did not fall.

The world has entered a long-term economic stagnation?

So, has the world entered a long-term economic stagnation? There is indeed a lot of evidence. Europe's unemployment rate is over 10%, growth is weak; overcapacity exists in many industries; inflation rate is below 2%; nominal wages have barely increased in all developed economies; interest rates have long been at historic lows; world population growth has been Slowly, several big countries have shown negative growth? All of this indicates that long-term economic stagnation has arrived.

On the other hand, the 2008 financial crisis and the subsequent economic recession have had a huge negative impact on the world economy. Compared with the recovery after 1945, the US economic recovery has been at a low point; the European recovery has been suspended due to the second recession in 2012, and the economic recovery in the European continent has been slower since then. Only time will tell whether we have entered a long-term economic stagnation or just a slow recovery after a serious economic shock.

In October 2015, the IMF believed that the world economy is gradually recovering, and the actual output growth rate exceeds the potential output. By 2020, the economic stagnation of the United States and Japan will be almost at the end. However, the IMF has always been considered too optimistic about its forecasts in recent years. We cannot know the long-term development direction of the next few years. The long-term current account surpluses of many large and medium-sized countries indicate that these countries lack investmentable projects and can only deal with their excess savings in a few other countries, especially in the United States. The investment ratio of some developed countries has declined, especially in Japan and the Eurozone, but the rest of the world has not seen much. However, the desired savings rate may be rising, in part due to the increase in capital stock and related depreciation subsidies, in part due to the extensive demographic changes mentioned above.

3

Where is the 1.7 trillion yuan going to the sea?

Author: season Grus exchange rate strategist at BNP Paribas (China) Co., Ltd.

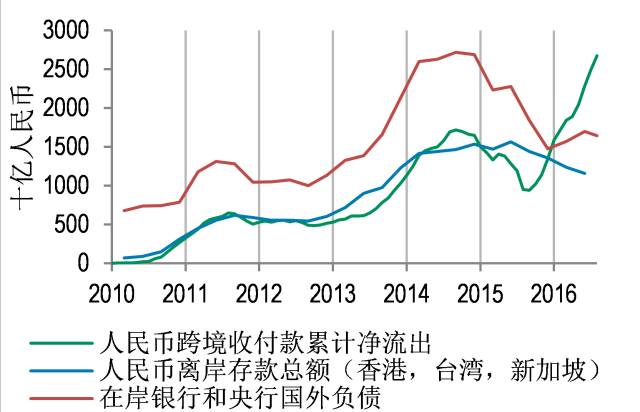

During the 11-month period from October last year to August this year, the RMB has been net outflows for 11 consecutive months, totaling 1.7 trillion yuan. The net outflow of RMB in this round is the third round of net outflow in history. The net outflow is the bank’s foreign exchange payment, which refers to the payment between the non-financial entity and the offshore entity on the shore, regardless of the onshore financial entity and offshore payment. In the past, the net outflow of RMB first made offshore finance and offshore non-financial increase in renminbi deposits. The renminbi deposits held by offshore finance were represented by the foreign liabilities of the central bank of the onshore bank. As can be seen in the figure below, the red, green and blue lines are consistent before 2015.

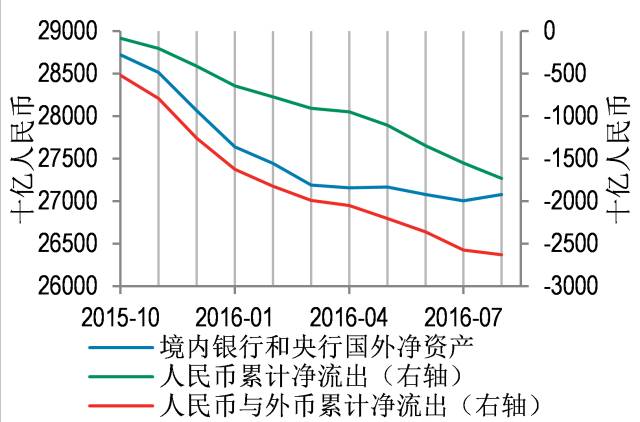

Now we see two deviations. The first is the deviation between the net outflow of RMB and the total amount of offshore RMB deposits, followed by the deviation of the net outflow of RMB and the foreign liabilities of domestic banks. Offshore non-financial no longer holds RMB assets in the form of offshore RMB deposits, but converts them into other assets upon receipt of RMB. Therefore, although offshore non-financials continue to receive RMB remittances, we do not see an increase in offshore RMB deposits, but even see a decline in offshore RMB deposits. The operation of offshore financial institutions is more complicated. We see a cumulative net outflow of RMB and foreign currencies, and a net good balance between domestic banks and foreign banks. In the two quarters from October 2015 to March 2016, there is a very good correspondence. In other words, the net outflow of RMB 900 billion during this period, together with the relatively large net outflow of foreign currency, has led to a decline in the net assets of domestic banks.

More specifically, the net outflow of foreign currency means that the foreign exchange of the central bank of the domestic bank is lost to the outside world, but there is no corresponding reduction in foreign debt, which leads to a decrease in the foreign net assets of the central bank of the domestic bank. The net outflow of RMB first means that the foreign bank's foreign debts increase, but since then, offshore finance has used this credit to the central bank of the domestic bank to withdraw the foreign exchange of the central bank's assets, thus returning the foreign debt of the domestic bank's central bank. The level before the net outflow of the renminbi, while the foreign exchange on the asset side of the central bank of the domestic bank was transferred, which also means that the foreign capital of the central bank of the domestic bank is reduced.

After considering the net outflow of 900 billion yuan, we will consider the net outflow of RMB 800 billion from April to August 2016. In the past five months, the net foreign currency inflow of 200 billion yuan, the direction and the net outflow of the renminbi, the scale is also small. At the same time, we saw that the foreign bank's foreign net assets fell by 112 billion, which means that of the net outflow of 800 billion yuan, there may be 300 billion yuan still used to withdraw foreign exchange. The remaining 500 billion yuan may be returned to the shore by other means.

For example, China Debt mentioned that in April, May, July and August 2016, foreign institutions bought a total of 200 billion yuan in bonds. In the future, as the RMB joins the SDR and the possible onshore bond market is included in the global bond index, the demand for RMB by foreign securities investors is expected to increase, and the return of the RMB may be stronger. However, this is a game between offshore financial institutions and onshore financial institutions, and it may not be related to offshore non-financial entities. Therefore, this return is not reflected in the foreign exchange receiving and payment.

All in all, the net outflow of RMB in this round is different from the net outflows in the first two rounds. The RMB is not held in offshore form by offshore finance and offshore non-financial. Secondly, the current round of RMB net outflow is divided into two stages: in the first stage, the net outflow of RMB is a way for the central bank's central bank to lose foreign exchange, corresponding to the reduction of foreign bank's net assets in the domestic bank; in the second stage, part of the net outflow of RMB It was reinvested offshore by the offshore bank and was not used to exchange foreign exchange from the central bank of the domestic bank.

From the above discussion we can draw some inferences. First, the idea of ​​observing offshore renminbi deposits to judge offshore renminbi funds is no longer applicable to the current offshore renminbi market. The reduction of offshore renminbi deposits can only indicate that offshore non-financial entities have a decline in interest in the renminbi and does not reflect the demand for renminbi by offshore financial entities. As the role of offshore finance becomes increasingly important, only pegged offshore renminbi deposits will miss an important part of the offshore renminbi market.

On the other hand, if we only pay attention to the cross-border movement of foreign exchange and ignore the cross-border movement of the renminbi, it will leave loopholes in the cross-border flow of capital. The foreign exchange bureau also noted the above issues. In the Balance of Payments Report for the first half of 2016, the SAFE noted that the proportion of inter-bank transactions in the entire foreign exchange market in the first half of 2016 increased from 75.4% in 2015 to 80.2%; the proportion of non-financial customer transactions was 23% fell to 18.9%, and pointed out that the substitution effect generated by the development of cross-border RMB settlement business may be an important reason. This observation is undoubtedly a matter of cut.

At present, the net outflow of RMB in a single month is 200 billion yuan, which is quite impressive compared to the offshore RMB market of 1.5 trillion to 2 trillion. The static pool of the offshore RMB market from small to small has become a dynamic pool of big and big. The payment and payment on behalf of customers and the non-financial entities on the shore have become the living source of offshore RMB pools, while offshore financial entities are replacing offshore non-financial entities and become the main players in the offshore market. Renminbi re-investment in the purchase of RMB assets onshore can also be used to withdraw foreign exchange from the central bank of a domestic bank at some point.

This means that if the central bank can throw out 200 billion US dollars at the beginning of the year and basically absorb all the renminbi liquidity offshore, then at the current time, the central bank will put the US dollar offshore. While the financial entity remits the RMB to offshore purchases, the central bank actually trades counterparts through the offshore market and onshore counterparts. This means that in the offshore market, the central bank throws out the dollar and the RMB is from the onshore main body. The size of the renminbi held by the onshore mains is a trillion.

The increased difficulty of central bank intervention does not mean that there will be more opportunities to short the RMB offshore. Offshore renminbi shorts need to worry about three aspects: First, the renminbi outflow from non-financial entities on the shore is reduced, second, the central bank intervenes offshore, and third, foreign central bank funds continue to put offshore renminbi back to shore. If the previous non-financial counterparts and offshore renminbi shorts face the central bank together, then the central bank has now gained the help of other central banks and investors entering the renminbi market. The prospect of offshore renminbi shorts seems to be more bleak, offshore renminbi interest rates. Volatility is also likely to become the norm.

Forex headline ID: waihuitoutiao personal WeChat: whtt111

Work Shoes,Work Boots,Nonslip Shoes,Business Casual Shoe

Desay Group CO.,Ltd , https://www.desaygroup.com